Health Insurance Literacy

Reframed health insurance enrollment from "better materials" to "better translation" after stats showed time and sources don't predict understanding.

Problem Space

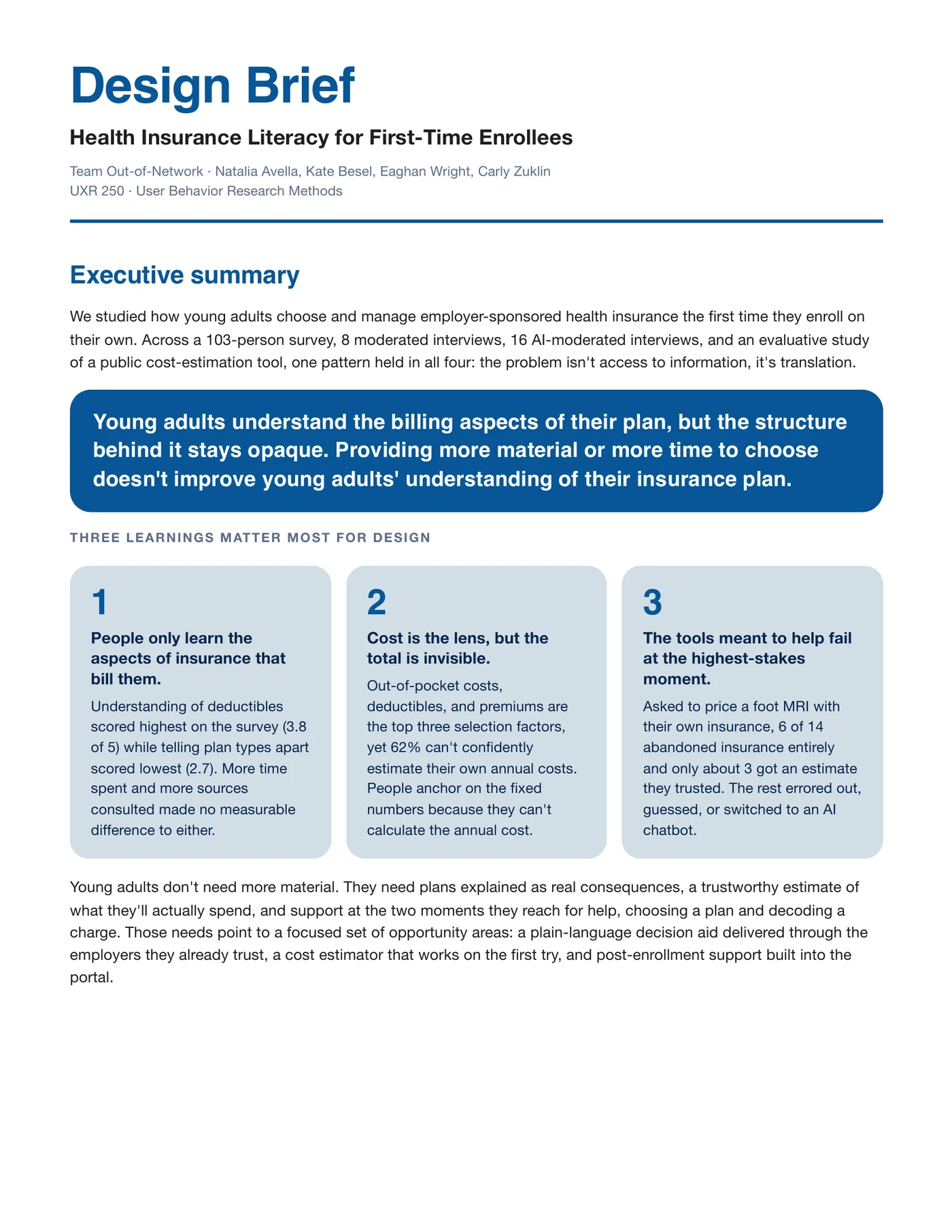

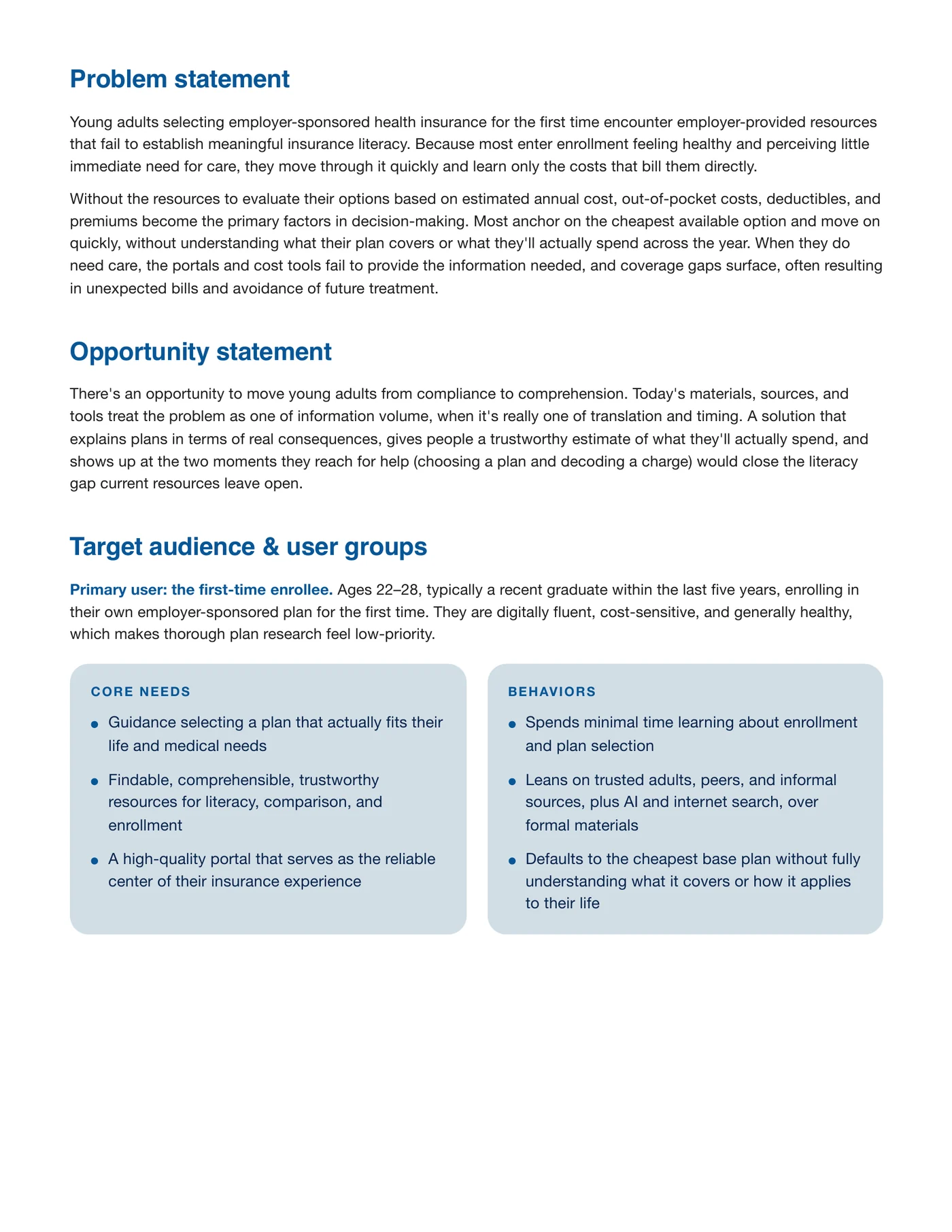

Young adults selecting employer-sponsored health insurance for the first time encounter employer-provided resources that fail to establish meaningful insurance literacy. Across our research — 103 survey respondents, 8 moderated interviews, 16 AI-moderated interviews, and 14 evaluative sessions on a public cost-estimation tool — one pattern held in all four methods: the problem isn't access to information, it's translation. Most enter enrollment feeling healthy, default to the cheapest available option, and discover the coverage gaps later as unexpected bills.

"I don't know the difference, and it doesn't really matter to me."

My Role & Constraints

My Role

Survey analysis lead and synthesis writer — built the statistical analysis pipeline, ran survey recruitment across 30 distributed channels, moderated 2 of the 8 in-person interviews, wrote the cross-method insights synthesis tying every interview theme to its survey evidence, and authored the team's 3-page design brief. I used AI to teach myself non-parametric statistics and to write the Python script.

Team

Natalia Avella, Eaghan Wright, Carly Zuklin. We developed our research plan and protocol as a team, coded the first two interviews independently, then built a shared codebook.

Constraints

Ten-week quarter. Open enrollment had already closed before fieldwork, so we couldn't observe selection live and instead ran a cognitive portal walkthrough to study how people use insurance resources post-enrollment. Our original strict screener forced a mid-quarter revisit.

Research Methods

Moving to a panel out of necessity, then testing AI moderation on purpose

Our original plan was 8–12 human-moderated interviews under a tight screener, but we only recruited 8 participants. We pivoted to a paid panel (Maze/Prolific) to scale recruitment and unblock the study. Instead of continuing human-moderated interviews, we switched to AI moderation after attending the UX360 research conference halfway through the quarter. Many of the sponsors are AI-moderated platforms, and we wanted to test them in our own study.

Since we had already collected insightful data from the 8 human-moderated sessions, we ran 16 AI-moderated sessions through Maze using two different AI workflows: structured (8) and unstructured (8). Structured used our scripted guide, and unstructured used general topics of interest. Structured hit the script but its probes were off-context, leading, or missing altogether. Unstructured probed better, but neither AI tier matched the nuance of a human moderator.

Cost dominates selection

The interviews surfaced "cost first" as a near-universal pattern. The survey showed the priority of each cost factor: out-of-pocket costs, deductibles, and premiums sat at the top, ahead of every coverage-quality measure.

Top Selection Factors

% of survey respondents

"Definitely the cost. Like, I chose the lowest cost."

Time and Sources Don't Predict Understanding

We expected that participants who spent more time researching or consulted more sources would be more confident and insurance-literate. But the survey analysis revealed that time didn't predict confidence, number of sources didn't predict literacy on any item, and the most common source — employer HR materials — produced no measurable lift over any other sources.

The interviews highlighted that participants treated their employer's materials as the trustworthy place to start, but described them as too complex or too surface-level to actually use. So they leaned on a parent, a coworker, or AI to translate the plans offered into something they could act on. I walked the team through the survey findings, and we synthesized the qualitative and quantitative data together, finding that the problem isn't engagement or effort, it's translation.

To test this further, we launched evaluative sessions where participants had step-by-step instructions to estimate the cost of an MRI using the Mayo Clinic cost calculator. Of the 14 participants, only 3 came away with an estimate they trusted, 6 gave up and continued without their insurance, and 2 errored out entering their details. Watching the tool fail in real time strengthened our survey and interview findings. Even with a script to follow and a calculator built for exactly this task, most couldn't reach a number they trusted. So when 62% of respondents said they couldn't confidently estimate their annual costs, the gap isn't effort or literacy, it's the tools. Unhelpful information, broken processes, and unreliable tools fail to create strong health insurance literacy and confident cost understanding.

Where We Expected a Correlation, We Found None

We expected three things to predict insurance literacy — time spent learning, number of sources consulted, and using employer HR resources. None of them did.

More time doesn't mean more confidence

Confidence stays flat across every time bucket.

More sources doesn't mean more literacy

Every correlation is near zero, on every literacy concept.

HR users score no higher than non-users

Identical medians on every literacy item.

Outcome

The research reframed the design surface.

"Young adults need better employer materials" became "young adults need plans explained as real consequences" — because more material doesn't close the literacy gap. The synthesis became the design brief's three learnings: people only learn the aspects of insurance that bill them, individual costs are the most important but the total cost is invisible, and the tools meant to help fail at the highest-stakes moment.

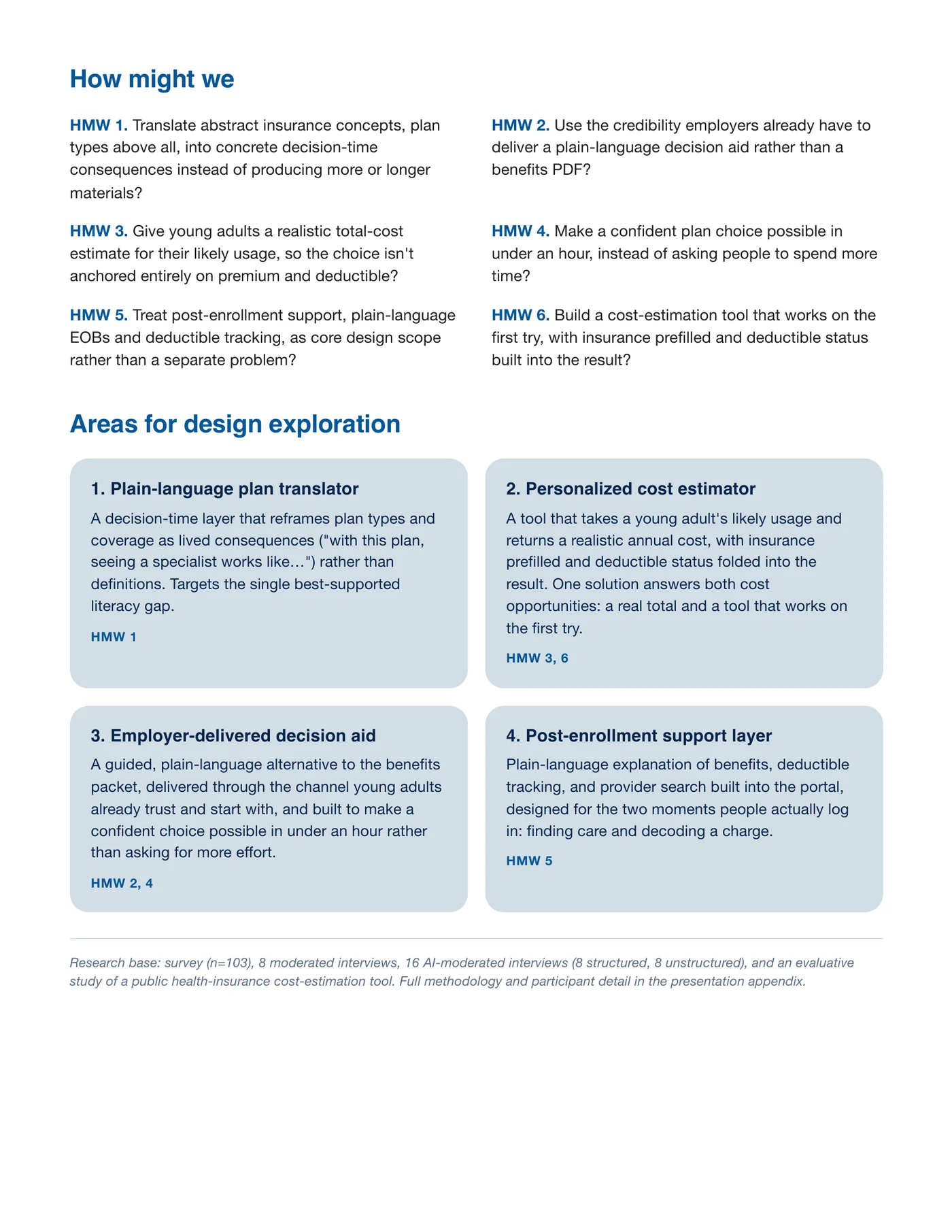

The brief turned those into six How Might We statements and four design-exploration areas — research-backed direction in an industry underserved by design.

The methods comparison produced its own conclusion: AI-moderated interviews are a viable scale lever for attitudinal data, but probe quality still lacks the nuance of human moderators.

Areas for Design Exploration

Four research-backed design opportunities, aimed at helping young adults understand and select a plan that matches their financial and care needs.

Plain-language plan translator

A decision-time layer that reframes plan types and coverage as lived consequences — "with this plan, seeing a specialist works like…" rather than definitions. Targets the single best-supported literacy gap.

HMW 1Personalized cost estimator

A tool that takes a young adult's likely usage and returns a realistic annual cost, with insurance prefilled and deductible status folded into the result. One solution provides a real total and a tool that works on the first try.

HMW 3, 6Employer-delivered decision aid

A guided, plain-language alternative to the benefits packet, delivered through the channel young adults already trust and start with, and built to make a confident choice possible in under an hour.

HMW 2, 4Post-enrollment support layer

Plain-language explanation of benefits, deductible tracking, and provider search built into the portal, designed for the two moments people actually log in: finding care and decoding a charge.

HMW 5Reflection

I'd rewrite the unstructured AI protocol to push deeper into the patterns our moderated interviews surfaced, rather than reusing the same guide. The second round of interviews could have produced genuinely new insights rather than a thinner version of the data we had already collected.

I'd also add a portal-experience item to the survey, since the qualitative portal frustrations sit interview-only right now and a survey-level signal would let me defend them at scale.